- Digitizing the Technical Dashboard

- The Data Normalization Layer

- Trend-Following Algorithm Framework

- Mean Reversion Algorithm Framework

- Combating Look-Ahead Bias

- Multivariate Signal Convergence

- Automated Execution Handlers

- Hard-Coding the Risk Matrix

- The Perils of Over-Optimization

- Strategic Synthesis

Digitizing the Technical Dashboard

Algorithmic trading using technical indicators is the process of translating visual chart patterns into Boolean logic ($True$ or $False$). While a human looks at a chart and "feels" that a stock is overbought, an algorithm identifies that the Relative Strength Index (RSI) has exceeded 80 and the price is $> 2$ standard deviations from the VWAP.

The transition from manual to algorithmic requires Quantification. Every subjective term used in technical analysis—"strong trend," "exhaustion," "support"—must be assigned a specific numerical threshold. This quantification allows for Vectorized Backtesting, where the system can process 20 years of tick data in minutes to determine if a strategy actually possesses alpha or is merely a product of random variance.

The Data Normalization Layer

Before an algorithm can calculate an indicator, it must ensure data integrity. In algorithmic systems, the most common error is acting on Dirty Data (e.g., stock splits, dividend gaps, or "bad ticks").

Algorithm Input Checklist:

- Survivorship Bias: Ensure the test universe includes companies that went bankrupt.

- Adjusted Prices: Use prices adjusted for splits and dividends to maintain moving average continuity.

- Point-in-Time Stamps: Use data as it appeared at the moment of the trade, not as it appears now (revised data).

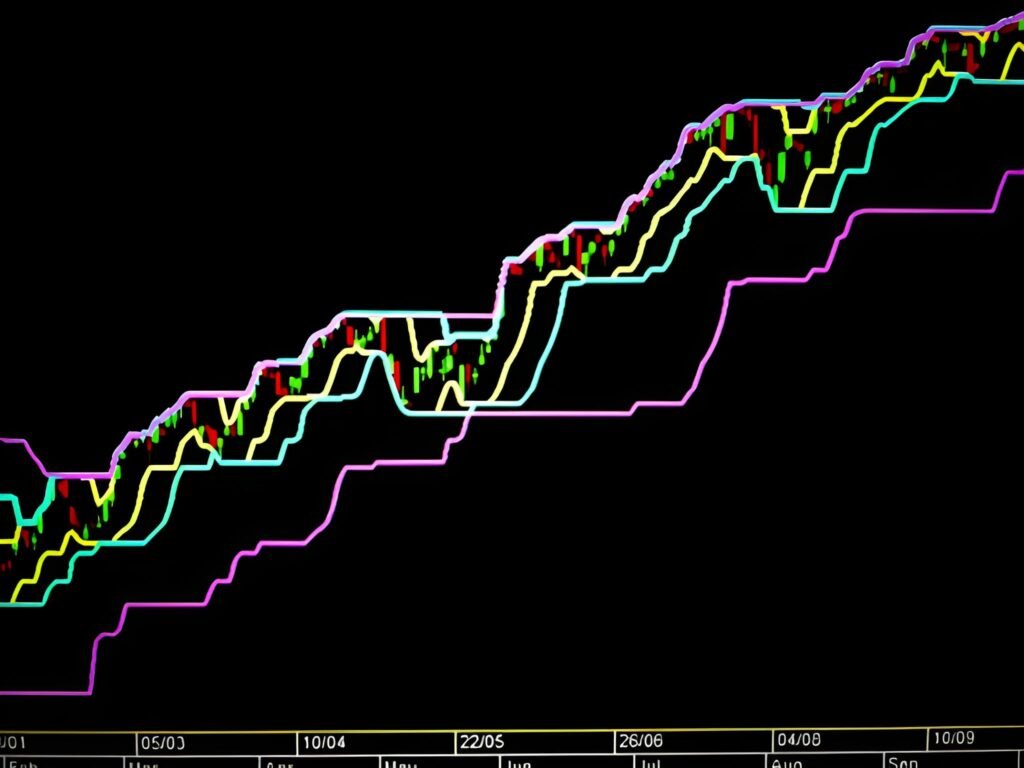

Trend-Following Algorithm Framework

Trend-following algorithms exploit Inertia (ref: momentum_factor_analysis.html). They are designed to enter after a move has started and exit when the velocity slows.

Golden Cross Logic

Buy if $SMA_{50} > SMA_{200}$ and $Price > SMA_{50}$. This filters out short-term noise and positions the algorithm in a confirmed macro trend.

ADX Strength Filter

Reject all signals if $ADX(14) < 25$. This ensures the machine only trades when the market has transitioned from a range to a trend.

Mean Reversion Algorithm Framework

Mean reversion algorithms exploit Entropy. They identify statistical extremes and bet on a return to the average (ref: mean_reversion_options.html).

| Indicator Condition | Algorithmic Interpretation | Automated Action |

|---|---|---|

| $Price < Lower Bollinger Band(20, 2)$ | Statistical Oversold | Generate Long Signal. |

| $RSI(2) < 10$ | Acute Exhaustion | Increase Signal Weight. |

| $Price \approx VWAP$ | Equilibrium Reached | Trigger Automated Exit. |

Combating Look-Ahead Bias

In algorithmic backtesting, "Look-Ahead Bias" is the silent killer. It occurs when your code inadvertently uses future information to make a past decision.

The Shift(1) Protocol

When coding an algorithm in Python, you must always "shift" your signals by one period. If the RSI crosses 70 on Candle $T$, you can only execute the sell at the open of Candle $T+1$. Failing to do this results in "unrealistic" win rates and catastrophic failure in the live market.

Multivariate Signal Convergence

Single-indicator algorithms are fragile. Professional desks use Signal Convergence—requiring multiple distinct indicator types to agree before a trade is fired.

- The Trigger: An EMA Crossover (Momentum).

- The Qualifier: RVOL > 2.0 (Volume Validation).

- The Guardrail: ADX > 25 (Regime Confirmation).

The machine only hits the order book when the Logical AND gate for all three conditions returns $True$.

Automated Execution Handlers

The algorithm's signal is useless without a precision Execution Module (ref: electronic_trading_fundamentals.html). For momentum-based indicator algos, speed is the differentiator.

The Limit Offset Tactic: To ensure a fill during a technical breakout, the algorithm places a Marketable Limit Order. It calculates the current Ask and adds an "offset" (e.g., $0.05$). This guarantees a fill while preventing the algorithm from buying the absolute top of a news spike.

Hard-Coding the Risk Matrix

The machine does not have "hope." Risk management in an algorithm must be hard-coded into the Order Management System (OMS).

The Algorithmic Risk Stack:

1. Fixed-Fractional Sizing: Automatically calculate shares based on 1% risk of current NAV.2. Trailing Stop: Move stop-loss higher for every ATR expansion in price.

3. Time-Stop: Exit if the technical indicator signal has not reached Target X within $N$ minutes (Velocity decay).

The Perils of Over-Optimization

Traders often fall into the trap of "Curve Fitting." By tweaking indicator periods (e.g., changing a 14-period RSI to 13.5 to make the backtest look better), you are finding noise, not alpha.

Walk-Forward Analysis: To prevent this, professional quants use "Out-of-Sample" testing. They train the algorithm on 70% of the data and test it on the remaining 30%. If the performance drops significantly on the new data, the algorithm is over-optimized and will fail in the live market.

Algorithmic trading using technical indicators transforms the "Art" of trading into a "Science" of execution. By moving from visual patterns to verifiable data streams, you align your strategy with the mechanical reality of the modern market.

Success requires a commitment to Backtesting Integrity and Rigorous Risk Management. The machine is only as good as the logic you provide it. Respect the look-ahead bias, avoid curve-fitting, and always ensure your algorithm has a fundamental reason for the trade. In the world of automated finance, the trend is not just your friend—it is a mathematical probability that must be captured with clinical precision.