As a finance expert, I often get asked about the best way to grow wealth rapidly. One approach that stands out is an aggressive asset allocation mix. This strategy prioritizes high-growth assets like stocks, real estate, and alternative investments while minimizing exposure to safer, low-yield options like bonds and cash. But is it right for you? Let’s break it down.

Table of Contents

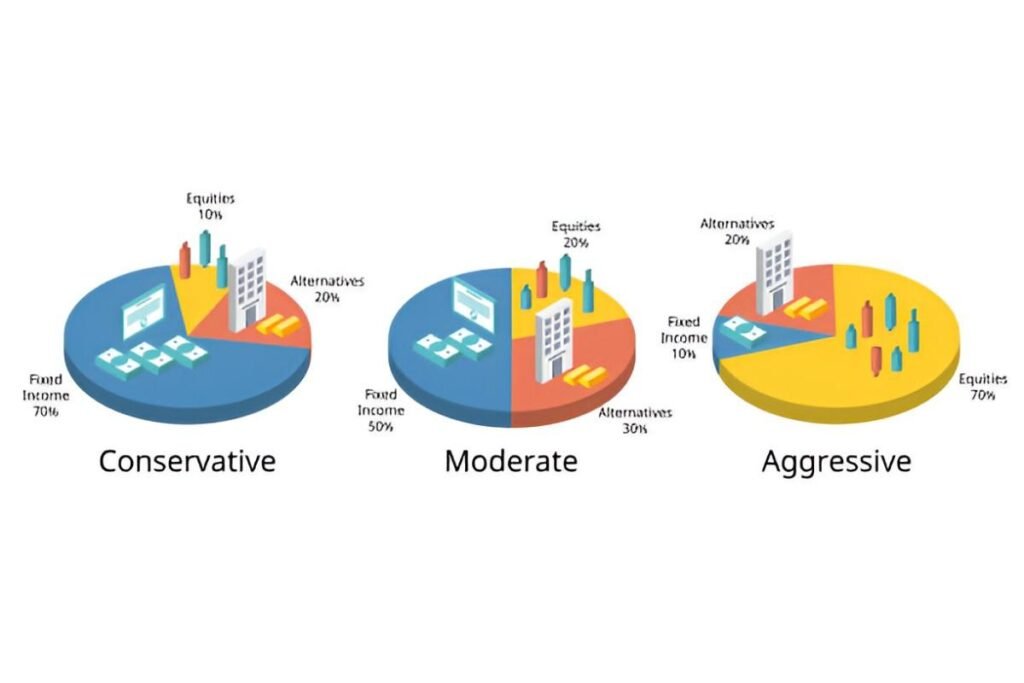

What Is an Aggressive Asset Allocation Mix?

An aggressive asset allocation mix is a portfolio strategy where the majority of investments are in high-risk, high-reward assets. Typically, this means:

- 80-100% in equities (stocks)

- 0-10% in fixed income (bonds)

- 0-10% in cash or equivalents

- Possible exposure to alternative investments (real estate, commodities, cryptocurrencies)

The goal is to maximize long-term returns, accepting higher volatility in exchange for growth potential.

Historical Performance of Aggressive Portfolios

Looking at historical data, the S&P 500 has delivered an average annual return of around 10% before inflation. Compare this to bonds, which have averaged 4-6%, and cash, which barely keeps pace with inflation.

\text{Expected Return} = \sum (w_i \times r_i)Where:

- w_i = weight of asset i in the portfolio

- r_i = expected return of asset i

For example, if you allocate 90% to stocks (10% return) and 10% to bonds (5% return), your expected return would be:

(0.90 \times 0.10) + (0.10 \times 0.05) = 0.095 \text{ or } 9.5\%Risk vs. Reward: The Trade-Off

While aggressive portfolios can generate higher returns, they come with significant volatility. During market downturns, a 100% stock portfolio could lose 30-50% of its value in a short period. If you panic and sell, you lock in those losses.

Standard Deviation as a Risk Measure

\sigma_p = \sqrt{\sum_{i=1}^n w_i^2 \sigma_i^2 + \sum_{i=1}^n \sum_{j \neq i}^n w_i w_j \sigma_i \sigma_j \rho_{ij}}Where:

- \sigma_p = portfolio standard deviation

- \sigma_i, \sigma_j = standard deviations of assets i and j

- \rho_{ij} = correlation coefficient between assets i and j

A well-diversified aggressive portfolio can mitigate some risk, but it will still be more volatile than a conservative one.

Who Should Use an Aggressive Asset Allocation?

Not everyone can stomach the ups and downs of an aggressive portfolio. Here’s who it might suit:

- Young investors (20s-40s): Long time horizon allows recovery from downturns.

- High-risk tolerance individuals: Those who won’t panic-sell during crashes.

- Investors with stable income: If you don’t need the money soon, volatility matters less.

Example: A 30-Year-Old’s Aggressive Allocation

| Asset Class | Allocation (%) | Expected Return (%) |

|---|---|---|

| US Stocks | 60 | 10 |

| International Stocks | 25 | 11 |

| Emerging Markets | 10 | 12 |

| REITs | 5 | 8 |

Using the expected return formula:

(0.60 \times 0.10) + (0.25 \times 0.11) + (0.10 \times 0.12) + (0.05 \times 0.08) = 10.35\%This mix balances growth potential while diversifying across geographies and sectors.

Common Mistakes in Aggressive Asset Allocation

1. Overconcentration in a Single Sector

Putting everything into tech stocks, for example, increases risk. Diversification is key.

2. Ignoring Rebalancing

Over time, winners grow and skew your allocation. Rebalancing ensures you stay on track.

3. Underestimating Emotional Reactions

Many investors abandon their strategy during downturns, turning paper losses into real ones.

Alternatives to Pure Equity Aggression

If 100% stocks feel too extreme, consider:

- Leveraged ETFs: Amplify returns (and risks) using financial derivatives.

- Private Equity/Venture Capital: Higher growth potential but illiquid.

- Real Estate Crowdfunding: Diversify beyond public markets.

Final Thoughts

An aggressive asset allocation mix can be a powerful wealth-building tool, but it demands discipline and a long-term mindset. If you can handle the volatility and have decades before retirement, the rewards may justify the risks. However, if market swings keep you up at night, a more balanced approach might be better.