As a finance professional, I often see investors make the same mistake—they chase returns without considering risk. The truth is, asset allocation matters more than stock picking or market timing. How you divide your portfolio between stocks, bonds, and other assets determines most of your long-term returns and risk exposure. In this guide, I’ll break down how to allocate assets based on risk tolerance, with practical examples, mathematical models, and real-world applications.

Table of Contents

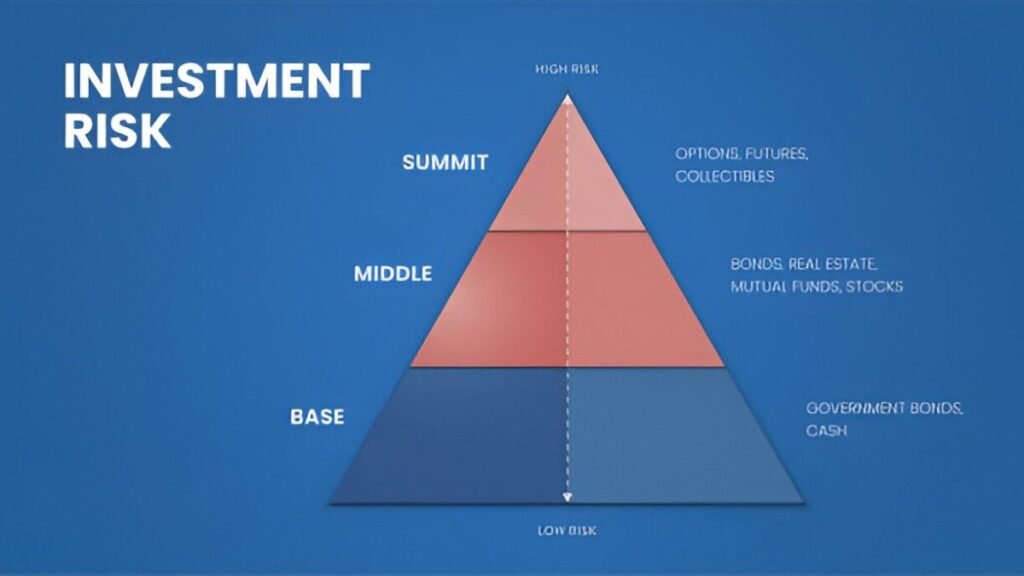

Understanding Risk Tolerance

Risk tolerance measures how much volatility an investor can stomach. Some people panic when markets drop 10%, while others stay calm during a 30% crash. Your risk tolerance depends on three key factors:

- Time Horizon – Younger investors can afford more risk because they have decades to recover. Retirees need stability.

- Financial Goals – Saving for a house in five years requires a different strategy than retirement in thirty years.

- Psychological Comfort – If market swings keep you awake at night, you’re taking too much risk.

Measuring Risk Tolerance

Financial advisors often use questionnaires to assess risk tolerance. A simple method is the “Rule of 100”:

Stock\ Allocation = 100 - AgeFor example, a 30-year-old would allocate 70% to stocks and 30% to bonds. However, this rule is outdated due to longer lifespans. A better version is the “Rule of 110 or 120”:

Stock\ Allocation = 120 - AgeA 40-year-old would then hold 80% in stocks. While useful, this rule ignores personal circumstances. A more precise approach uses Modern Portfolio Theory (MPT).

Modern Portfolio Theory and Efficient Frontier

Harry Markowitz’s MPT shows how diversification reduces risk without sacrificing returns. The core idea is that assets don’t move in perfect sync. When stocks fall, bonds often rise, smoothing out volatility.

The Efficient Frontier is a set of optimal portfolios offering the highest expected return for a given risk level. Mathematically, portfolio return E(R_p) and risk \sigma_p are calculated as:

E(R_p) = \sum_{i=1}^{n} w_i E(R_i) \sigma_p = \sqrt{\sum_{i=1}^{n} \sum_{j=1}^{n} w_i w_j \sigma_i \sigma_j \rho_{ij}}Where:

- w_i = weight of asset i

- E(R_i) = expected return of asset i

- \sigma_i = standard deviation (risk) of asset i

- \rho_{ij} = correlation between assets i and j

Example: Two-Asset Portfolio

Assume:

- Stocks: E(R) = 10\%, \sigma = 15\%

- Bonds: E(R) = 4\%, \sigma = 5\%

- Correlation (\rho) = -0.2

For a 60/40 stock/bond mix:

E(R_p) = 0.6 \times 10\% + 0.4 \times 4\% = 7.6\% \sigma_p = \sqrt{(0.6^2 \times 0.15^2) + (0.4^2 \times 0.05^2) + (2 \times 0.6 \times 0.4 \times -0.2 \times 0.15 \times 0.05)} \approx 8.7\%This portfolio has lower risk than a 100% stock allocation while still delivering solid returns.

Asset Allocation Models Based on Risk

Below are five common risk-based allocation strategies:

1. Conservative (Low Risk)

- Stocks: 20-40%

- Bonds: 50-70%

- Cash: 10-20%

- Best for: Retirees, short-term goals

2. Moderate (Medium Risk)

- Stocks: 50-70%

- Bonds: 30-50%

- Cash: 0-10%

- Best for: Mid-career professionals

3. Aggressive (High Risk)

- Stocks: 80-100%

- Bonds: 0-20%

- Cash: 0%

- Best for: Young investors with long horizons

4. Glide Path (Target-Date Funds)

Automatically shifts from stocks to bonds as retirement nears. Example:

| Age | Stocks | Bonds |

|---|---|---|

| 30 | 90% | 10% |

| 50 | 70% | 30% |

| 65 | 50% | 50% |

5. Risk Parity

Allocates based on risk contribution rather than capital. Uses leverage to balance volatility across assets.

Behavioral Pitfalls in Asset Allocation

Even with a perfect plan, investors often sabotage themselves. Common mistakes:

- Recency Bias – Overweighting recent winners (e.g., tech stocks in 2021).

- Loss Aversion – Selling in a panic during downturns.

- Overconfidence – Taking excessive risks after a few wins.

A disciplined, rules-based approach prevents emotional decisions.

Final Thoughts

Asset allocation isn’t a one-time decision. Rebalance annually to maintain your target mix. If stocks surge, sell some to buy bonds. If stocks crash, do the opposite. This forces you to “buy low, sell high” systematically.